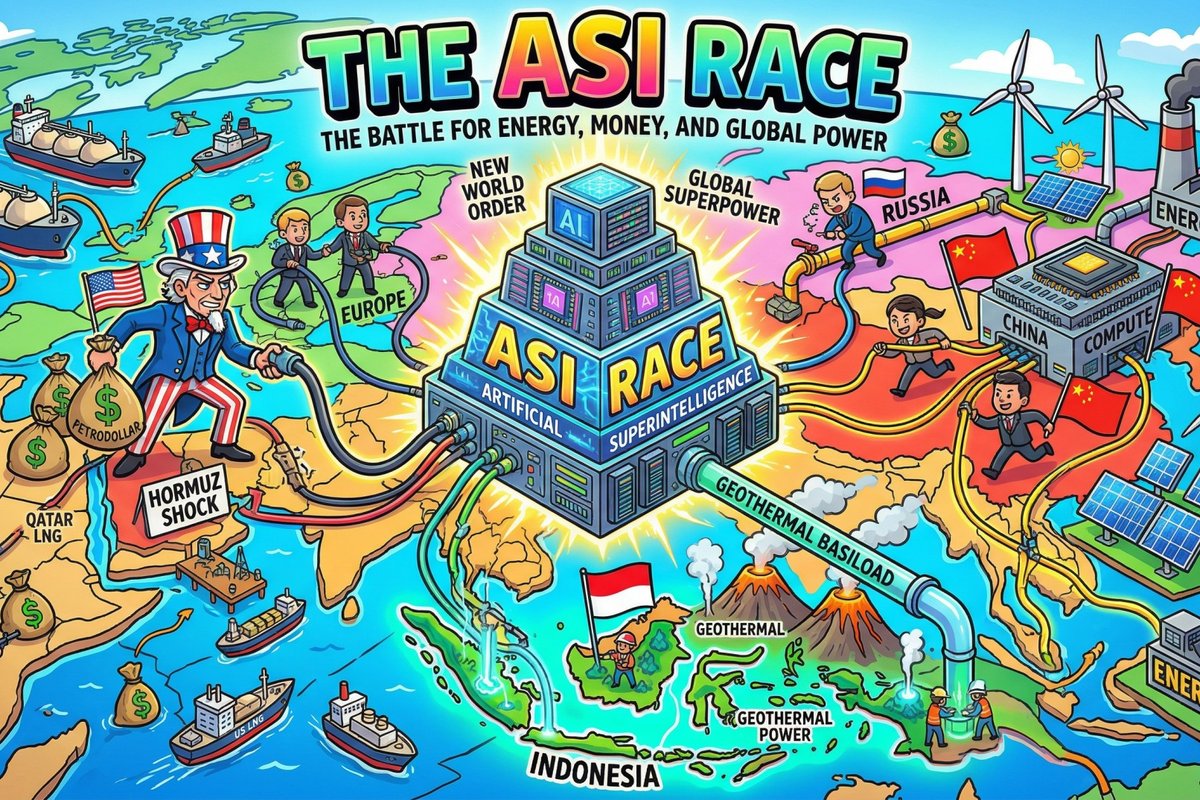

For years, artificial intelligence was marketed as if it lived in a pristine digital cloud, floating above the messy realities of geopolitics, pipelines, and power plants. That version of the story is convenient. It is also wrong in the most expensive way possible. The pursuit of Artificial Superintelligence (ASI) is not a software race. It is an infrastructure war.

The International Energy Agency projects that data center electricity demand will reach approximately 945 TWh by 2030. To put that massive figure into perspective, it is roughly equivalent to the entire annual electricity consumption of an industrialized nation like Japan. That means the real competition is not only about who writes better code. It is about who can supply the most reliable energy, the deepest capital, and the most resilient infrastructure to keep the machines running.

To understand how we arrived at this point, you have to start with the petrodollar.

For decades, the global energy system revolved around a simple but powerful structure. Oil was priced in U.S. dollars, traded in U.S. dollars, and recycled back into U.S. financial markets. This created a permanent feedback loop. Countries needed dollars to buy energy, making the act of holding dollars a strategic imperative. The dollar became the backbone of global trade not just because of financial strength, but because global energy demand forced it.

This was global architecture. Then, the system evolved. The world did not move away from the petrodollar. It upgraded it into the petro-LNG order.

Unlike crude oil, Liquefied Natural Gas (LNG) is not easily rerouted mid-ocean with a phone call. It requires multi-billion dollar liquefaction plants, specialized cryogenic carriers, and dedicated regasification terminals. Most importantly, it requires strict 15- to 20-year "take-or-pay" contracts, typically denominated in dollars. When countries build LNG terminals, they are not just buying fuel. They are locking themselves into a long-term physical and financial relationship.

Europe is the clearest example of this transformation. After the Ukraine war, Europe rapidly reduced its dependence on Russian pipeline gas. But in doing so, it did not become free; it became re-anchored. The United States stepped in as the dominant LNG supplier, providing roughly 60 percent of EU LNG imports by early 2026. Europe signed long-term contracts, replacing pipeline dependence with LNG dependence. It is more flexible politically, but far less flexible physically.

This rigidity exposes the fragility of the entire system. Military strikes on Iran's South Pars gas field and retaliatory disruptions affecting Qatar's LNG infrastructure removed roughly 17 percent of Qatar's export capacity in early 2026, with recovery timelines stretching years. The Strait of Hormuz, one of the most critical energy chokepoints in the world, became unstable.

Because LNG is contract-based and infrastructure-bound, disruptions ripple through long-term supply chains and industrial planning. When Hormuz is unstable, global market confidence halts. Energy becomes pure leverage. Whoever controls the supply, the routes, and the currency gains disproportionate influence over the global economy.

Now, layer Artificial Intelligence on top of this fragile system.

AI is a physical entity with extreme power density. Traditional server racks consumed 10 to 15 kilowatts. Modern AI training infrastructure has shattered that paradigm. High-density racks, such as those housing the NVIDIA GB200 NVL72, consume up to 120 kilowatts each and mandate direct-to-chip liquid cooling. This is no longer a software scaling problem. It is a thermodynamic bottleneck. The compute furnace demands energy constantly.

Building ASI is capital intensive on a historic scale. OpenAI is targeting roughly $600 billion in compute spending through 2030, while Big Tech collectively invests hundreds of billions annually. This money aggressively secures land, dedicated high-voltage transformers, water rights, and long-term Power Purchase Agreements.

The primary bottleneck is no longer silicon chips. It is grid capacity.

Servers can be manufactured and deployed in a few months. Transmission infrastructure cannot. High-voltage substations and grid interconnections can take up to a decade to permit and build. The real constraint on ASI is heavy infrastructure.

This is exactly why the type of energy matters.

AI requires near 100 percent uptime, a metric known as capacity factor. Solar and wind typically operate between a 20 to 30 percent capacity factor. Stabilizing them for continuous baseload requires massive, cost-prohibitive utility-scale battery storage. Geothermal energy, however, operates above a 90 percent capacity factor. It is stable, predictable, and always on. In the ASI era, geothermal is strategic sovereign power.

This is where Indonesia enters the story in a very serious way.

Holding one of the largest geothermal reserves in the world (estimated at 23.74 GW) Indonesia has the rare ability to produce sovereign, domestic baseload power without relying on imported LNG or coal. Indonesia is already seeing the physical manifestation of the ASI race through the development of massive, AI-ready hyperscale data center campuses. Industrial corridors, such as Jababeka, are increasingly being positioned to host expansive 600-megawatt hyperscale developments. These industrial compute zones are designed explicitly for the power density of superintelligence, requiring integrated digital decarbonization solutions to meet global tech's green mandates.

But there is a catch: Indonesia's energy is geographically fragmented.

The main demand center, the Java-Bali grid, still relies heavily on coal. Meanwhile, the vast geothermal resources are hidden across the archipelago in regions like Sumatra and Sulawesi. The true challenge is transmission. To become an ASI infrastructure hub, Indonesia must invest heavily in grid modernization, including high-voltage direct current (HVDC) transmission lines and subsea cables to move firm power across islands.

Funding this requires a blended financial model. State-backed grid investments must merge with foreign direct investment, multilateral financing, and long-term agreements with hyperscalers. In simple terms, the tech giants desperate for the power will help pay for the wires. Meanwhile, nuclear energy sits in the background as Indonesia's deep future bet for the 2030s, offering the ultimate long-term scale.

So where is the best place to build ASI data centers?

Not where land is cheapest. Not where policy is loudest. The winners will be where power is stable, scalable, and politically secure. Today, the United States and China lead. But in the next phase, countries like Indonesia become highly strategic if they can successfully convert their raw geothermal potential into reliable transmission networks that feed hyperscale campuses.

In the end, the ASI race is about physical systems. Energy feeds compute. Compute drives intelligence. Intelligence creates power. Power reshapes the world order.

The petrodollar was phase one. Petro-LNG is phase two. ASI is phase three. The winners will not just build smarter machines. They will build the physical civilization that those machines run on.