From Hormuz to Malacca, the winners of this era will be the countries that control energy flows, carbon storage, and the infrastructure behind artificial superintelligence, or ASI..

By: Rezky A. Supriadi

LinkedIn Profile

The fighting in the Gulf is loud, but the volume is misleading. Missiles, naval maneuvers, and warnings dominate headlines, yet they obscure a deeper reality. This is not just a conflict between states. It is a contest over the arteries of the global economy.

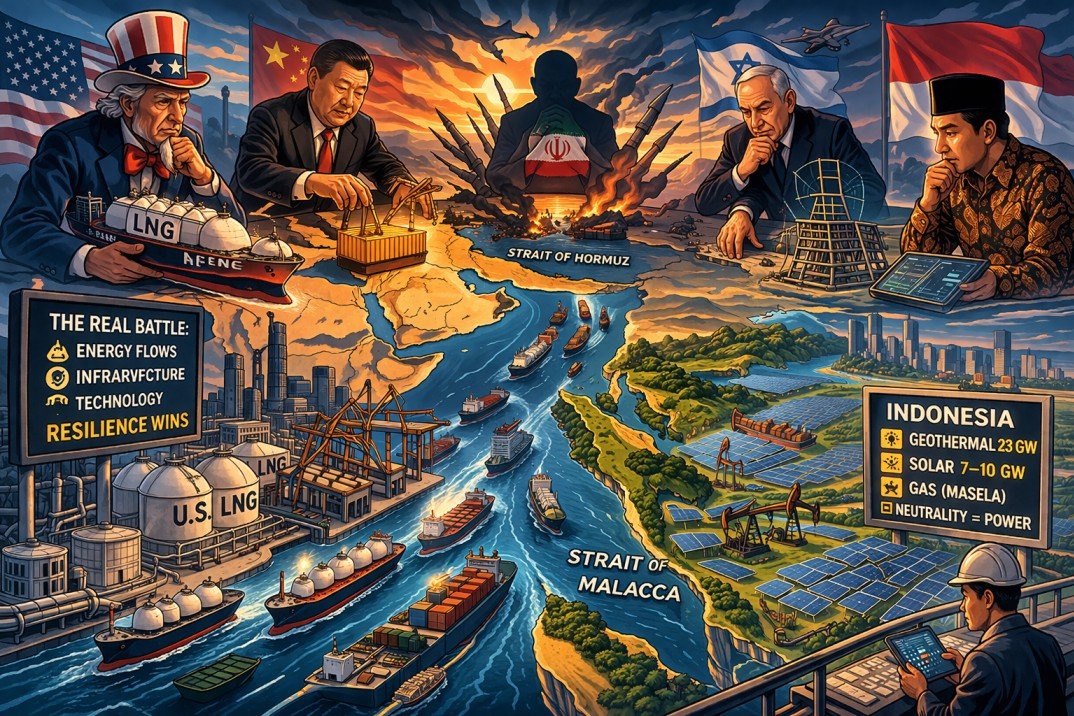

The Strait of Hormuz remains one of the world’s most critical chokepoints, carrying roughly one fifth of global oil and significant LNG flows. When instability threatens that corridor, the impact is immediate. Energy prices move, insurance costs rise, and supply chains tighten. The modern world still depends on a handful of narrow passages, and whoever influences them holds disproportionate leverage.

This is why the conflict matters beyond the region. The visible story is retaliation. The real story is continuity. Who can keep energy moving when the system is under stress.

The United States has positioned itself as a provider of that continuity. Its strength is not only military presence, but its role in global energy supply. American gas abundance comes from shale and associated gas, especially from basins like the Permian, Appalachia, and Haynesville. According to the U.S. Energy Information Administration, these regions dominate U.S. production, which has reached record levels.

But the advantage is not just about volume. It is about structure. U.S. LNG contracts are typically long term, often linked to Henry Hub pricing, and designed with destination flexibility. Buyers can redirect cargoes, hedge risk, and adapt to disruption. In an uncertain world, flexibility becomes as valuable as price.

That is the U.S. play. Not dominance through the cheapest energy, but through the most reliable and adaptable supply.

China is playing a different game. Instead of confronting instability, it builds around it. Guided by the logic of Sun Tzu, China focuses on infrastructure and long-term positioning. Through the Belt and Road Initiative, it has financed ports, railways, power systems, and digital networks across more than 130 countries.

This approach does not depend on winning conflicts. It depends on outlasting them. When one route is disrupted, another remains. When one system weakens, another continues. China’s strength lies in building systems that survive instability.

Iran sits in a constrained role. Its leverage comes from disruption, not stability. Control over access to the Strait of Hormuz allows it to influence global energy flows, but this influence increases risk rather than reducing it. Its future is likely defined by persistence under pressure, not decisive victory.

Israel occupies a different position. It is emerging as a security specialist rather than a regional protector. Its strengths lie in missile defense, intelligence, and deterrence. Some Gulf states may cooperate with Israel, but this does not translate into a unified regional security system under its leadership.

Together, these roles form a pattern. The United States stabilizes, China builds, Iran disrupts, and Israel specializes. None fully control the system, but each shapes a layer of it.

This is where Indonesia becomes strategically important.

The Strait of Malacca is the primary energy corridor for Asia, linking Middle Eastern supply to East Asian demand. Indonesia sits at the center of this flow.

But geography alone is not power. It is potential.

For years, Indonesia has lived with quiet dependencies that reduce its freedom of action. Reliance on imported staples such as wheat shows how easily supply chains become leverage. Dependency builds slowly, then becomes expensive to escape.

Indonesia’s energy advantage is not one source. It is a stack. Solar potential is about 200,000 MW, geothermal about 23.9 GW, hydropower about 95 GW, biomass about 56.97 GW, with additional contributions from waste-to-energy and wind. This is not a shortage of resources. It is a shortage of execution.

There is also a practical opportunity hiding in plain sight. Using standard benchmarks, 10,000 hectares of former oilfield or brownfield land could host roughly 3 GW of solar capacity. Idle industrial land can be converted into power without competing for new space.

Syngas adds another layer. Coal, biomass, and waste can be converted into synthetic gas and fuels such as DME, reducing LPG imports. Waste-to-energy can turn urban waste into electricity instead of landfill burden. These are not glamorous solutions, but they are effective where it matters.

Then there is carbon storage. Depleted oil and gas reservoirs and saline aquifers can be used to store carbon at scale. Estimates suggest Indonesia has hundreds of gigatons of storage potential. This transforms old fossil infrastructure into future strategic assets and positions Indonesia as a potential regional carbon storage hub.

The next phase matters even more because the energy system is being pulled into the AI economy. The International Energy Agency projects global data center electricity demand could approach 945 TWh by 2030. This is not just growth. It is a structural shift. The countries that can provide reliable, continuous power will be the ones that matter most.

If Indonesia secures its energy base, reduces dependencies, and builds resilience across this stack, it can move from being a transit route to becoming a critical node in the global system.

The war in the Gulf will eventually quiet down. It always does. But the structural lesson will remain.

The real contest is not over territory. It is over the systems that keep the world running when disruption becomes normal.

And in that contest, the countries that matter most will not be the loudest.

They will be the ones the world cannot afford to lose.